Benefit in Kind changes for Company Cars

The Budget and Finance Bill have outlined the benefit in kind (BIK) percentages for company cars up to the tax years 2028/29 and 2029/30. While businesses can now plan over the next five years, they need to plan for an increase.

Key Points

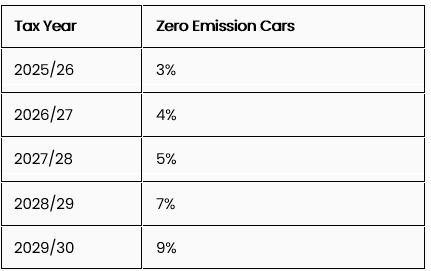

- Zero Emissions Cars (Pure Electric): BIK percentages will rise by 1% annually from 2025/26 to 2027/28, then by 2% annually to reach 7% in 2028/29 and 9% in 2029/30.

- Other Cars: BIK percentages will increase by 1% annually, capping at 38% in 2028/29 and 39% in 2029/30.

Detailed Breakdown for Zero Emission Cars

The upcoming changes in tax percentages for hybrid and pure electric cars could impact their attractiveness as company cars. Hybrid cars will see a significant increase in tax percentages, while pure electric cars will also face higher percentages but still offer some tax benefits.

Key Points

- Hybrid Cars: Tax percentages for hybrids with CO₂ emissions of 1–50g/km will be based on electric range until 2027/28. From 2028/29, all such hybrids will have a flat percentage of 18%, rising to 19% in 2029/30.

- Pure Electric Cars: Tax percentages will rise to 9% by 2029/30. The vehicle excise duty (VED) exemption ends in April 2025, but salary sacrifice remains effective, and first-year allowances are extended.

Detailed Breakdown for Pure Hybrid Cars

Detailed Breakdown for Pure Electric Cars

Considerations

- Hybrid Cars: Businesses may need to reconsider long-term leases or purchases due to the significant tax increase.

- Pure Electric Cars: Despite rising tax percentages, they remain competitive and offer tax savings through salary sacrifice and first-year allowances (until 31 March/5 April 2026 under current policy). However, practical concerns like charging infrastructure and VED costs should be considered.

Opting for a van instead of a car can be a cost-effective choice for company vehicles. However, there are important considerations, especially regarding double-cab pickups and upcoming tax changes.

Key Points

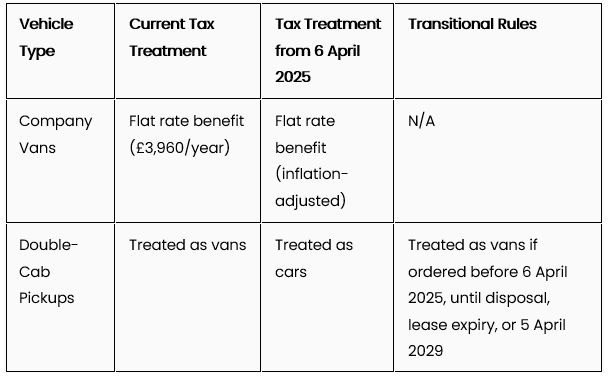

- Company Vans: Employees are taxed on a flat rate benefit (£3,960/year), which will increase from April 2025 to £4,020.

- Double-Cab Pickups: From 6 April 2025, pickups with a payload of one tonne or more will be treated as cars for tax purposes. Transitional rules apply for vehicles ordered before this date.

Detailed Breakdown

Considerations

- Company Vans: Generally result in a lower tax charge compared to company cars.

- Double-Cab Pickups: Businesses should act quickly to order before April 2025 to benefit from transitional rules.

- Future Planning: Businesses should consider upcoming tax changes to avoid surprises and may want to explore pure electric cars as an alternative.

Want to discuss Benefits in Kind?

Get in touch with Angela, tax director, and find out how we can help you today.